Getty Images/iStockphoto

Debunking 5 blockchain myths and misconceptions

There's more to blockchain development than what you hear from the crypto community. Here, we debunk five common blockchain myths.

Enterprises are investing billions of dollars in blockchain technology, but some persistent myths about the technology hamper faster blockchain adoption. Let's examine these five myths and set the record straight as to why they aren't true:

- Blockchain is an unsecured free-for-all.

- There's no privacy on the blockchain.

- Blockchain is only useful for cryptocurrency and cryptocurrency speculation.

- Blockchain is anti-government.

- Blockchain programming is too hard for mainstream developers.

1. Blockchain is an unsecured free-for-all

Blockchain is quite secure in many ways.

First and foremost, data added to the blockchain cannot be changed. Blocks on a blockchain are immutable. If, by some extreme possibility, existing data on a blockchain is changed, the entire blockchain is corrupted and deemed invalid.

Also, adding data to a blockchain is a complex undertaking. A significant majority of computers on the blockchain network, called nodes, must agree to add the particular block. A computing entity called a miner, also known as a validator, validates a block, and then the other nodes on the network agree on the validation. Remember that a blockchain network can be made up of hundreds, if not thousands of nodes.

Miners/validators are compensated for adding data to the blockchain. A miner/validator also must make a significant investment to participate in the blockchain. Two of the most popular techniques to do so are proof of work and proof of stake:

- Proof of work means a miner/validator devotes considerable computing power to be the first entity to validate and form a block to add the blockchain.

- Proof of stake means to invest money upfront for the right to verify and add data to the blockchain and be compensated accordingly. If a miner makes a mistake or hacks the system, that miner forfeits its investment.

Logically, those who invest a large sum of money upfront to participate in a node and blockchain validation would not risk that investment by attempting to hack the system.

It's important to understand that security on a blockchain is not defined by one party granting to another party access and permissions to the given blockchain. Rather, access and validation are granted according to principles and practices governed by processes which are essentially mathematical in nature.

2. There's no privacy on the blockchain

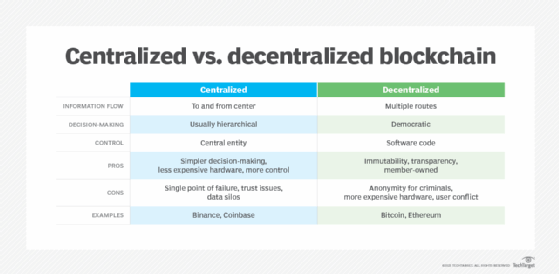

All blockchains work under a decentralized, peer-to-peer architecture. However, it is also possible to create blockchains that are private to a particular organization or group of users.

The core principle of blockchain technology is that all nodes on a blockchain network have the same data and act in concert to add new data. If any node on the blockchain network goes down, the entire blockchain is unaffected.

However, there is no rule that dictates that all blockchains must be exposed to the public. Some blockchains might be exposed to the public, others might not. Private blockchains are also referred to as permissioned blockchains -- an example of this is Corda.

Also, there is the matter of personal privacy. By definition, a well-known blockchain such as Bitcoin and Ethereum identifies users only by an address that is represented as a hexadecimal value. No personally identifiable information (PII) is stored as part of blockchain transactions; that information is stored elsewhere.

The key takeaway is that a blockchain can be either public or private. It all depends on the given blockchain's intended use and configuration.

3. Blockchain is only useful for cryptocurrency and cryptocurrency speculation

Blockchain is foundational to cryptocurrency -- and many people think of blockchain only in terms of cryptocurrency. This is understandable given the enormous attention that cryptocurrency gets in the media, with the dramatic rise and fall of fortunes made by way of cryptocurrency speculation and manipulation.

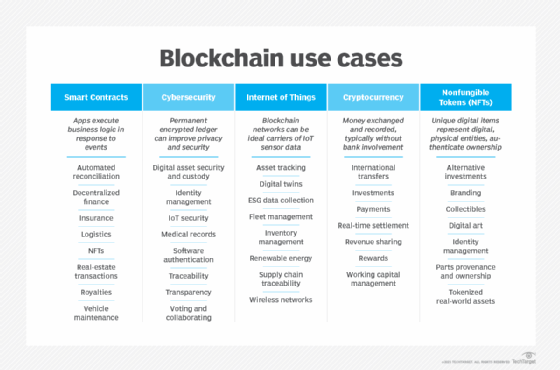

However, there are many uses for blockchain other than as a platform to support cryptocurrency.

Essentially, blockchain is a data storage mechanism. Beyond that, blockchain also has become a viable application platform thanks to the introduction of two related technologies:

- The non-fungible token (NFT), a particular type of data structure stored on a blockchain.

- Smart contracts, which provide a way of creating logic that is stored and executed on a blockchain.

This gives way to a vast number of use cases that go beyond cryptocurrency activities. In fact, these days distributed ledger technology is the term used to describe blockchain as a decentralized database.

Distributed ledger technology can be used for a wide variety of activities: supply chain management, distributed finance applications, marketing programs, gaming and motor vehicle administration.

4. Blockchain is anti-government

One of the first uses of blockchain was to create a digital currency that's not subject to government jurisdiction -- think Bitcoin. Today, though, many governments and agencies experiment with and endorse blockchain technologies for their own purposes.

The California Department of Motor Vehicles is experimenting with a project to put its titles on a private NFT-based blockchain. In 2020 the U.S. Food and Drug Administration (FDA) launched a pilot program with KPMG, IBM and Walmart to use blockchain technology to identify, track and trace prescription medicines and vaccines in the U.S.

Interest in blockchain goes beyond the U.S. government. The government of Germany published a comprehensive blockchain strategy in 2019 that paves the way to use blockchain in management and administrative activities. And the Monetary Authority of Singapore promotes the use of blockchain technology for commercial and government activities.

Blockchain technology has a wide variety of applications in both the private and public sectors. While some proponents of blockchain might have an anti-government leaning, the technology itself is agnostic.

5. Blockchain programming is hard for mainstream developers

You'd be hard pressed to find an enterprise software framework with no significant learning curve for programmers to overcome. It can take months or years to develop expertise with Kubernetes, for example. Learning to work with Spring, a popular framework for programming Java, is not accomplished in a week. The React framework for client-side web programming has a steep learning curve as well.

There's a learning curve for those who program for the blockchain, but in the scheme of things it's rather straightforward to get the hang of it.

The core entity for programming on the blockchain is the smart contract. Smart contracts that run on blockchains compatible with the Ethereum Virtual Machines (EVM) are typically written in the Solidity programming language. Solidity has many object-oriented qualities, so developers who understand Java, C# or TypeScript should easily adopt it.

Smart contracts for the Solana blockchain can be written in Rust, C, C++ or Python. The EOS blockchain supports C++ for creating smart contracts. Other blockchains support smart contract development as well.

Blockchain platforms want developer adoption, so they try to make it as easy as possible for developers to be productive. Many blockchain platforms use preexisting languages. Some use special languages, such as programming in Solidity for EVM-compatible blockchains. However, these languages should not be considered obstacles to adoption.

No matter what blockchain platform developers choose, they must understand how the particular blockchain works and how it's managed. The other half of their job is to become expert enough to do the coding for it. Yes, there is a learning curve to program for blockchain, but it is no steeper for a mainstream developer than learning a new programming language.

Blockchain is not useful for everything, but the technology is a viable platform for many commercial and governmental situations. The key to consider adopting blockchain technology is to rely on information based on facts rather than perceptions based on myths.